October is notoriously a volatile month for risk assets, and this year it marked a month the S&P 500 index crossed into correction territory (defined as a greater than 10% drop from a recent peak) with interest rates on U.S. Treasuries reaching multi-year highs. The S&P 500 index crossed the correction threshold intra-month but rallied in the final days of October to finish down 2% for the month and 9% from its mid-summer peak. The interest rate on the benchmark 10-year U.S. Treasury rose above 5% for the first time since 2007.

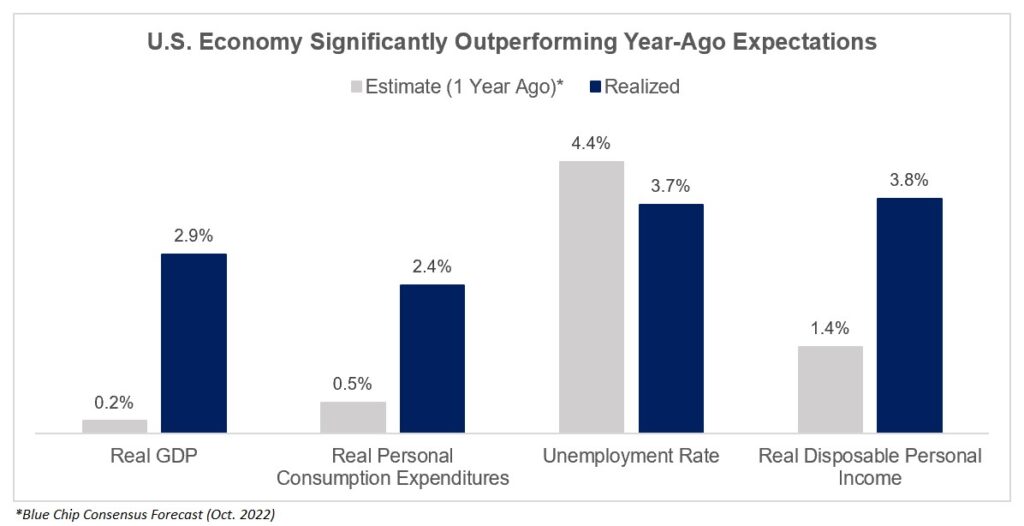

There were several factors in play, but investor focus continues to be on the future path for interest rates. U.S. economic data remains resilient. The monthly Labor Department Report showed the economy added 336k jobs in September (more than double expectations) with rising real wages. The third quarter GDP report showed real GDP grew at a 4.9% annual rate. Total personal consumption expenditures inflation was up 3.4% over the past twelve months, indicating the U.S. consumer continues to spend robustly. The prospect of “higher for longer” rates grew in consensus throughout the month as each incremental datapoint indicated the Fed may need to do more to reign-in inflation.

Outside of the interest rates narrative, geopolitical angst was exacerbated by the start of the Israel-Hamas war on October 7. We think impacts on the U.S. economy are relatively limited at this stage, but we are evaluating risks around a broadening of the conflict. Implications for global financial markets grow the longer the conflict persists, and this weighed on sentiment.

Lastly, third quarter earnings season is in full swing, with more than half of the S&P 500 reporting results in October. The S&P 500 is reporting year-over-year earnings growth for the first time since the third quarter of last year. Both the number and magnitude of earnings surprises are above their averages. However, a handful of high-profile disappointments contributed to outsized declines in certain companies and sectors.

Diversification does not eliminate risk of loss in market corrections; rather, correlation is the highest among risk assets in down markets. For this very reason, we are seeing unique opportunities in certain pockets of the market which have been unjustly hit by the correction and continue to pursue quality companies trading at attractive valuations. The forward price to earnings ratio of the S&P 500 is ~17x, below its 5- and 10-year average P/Es of ~19x and ~18x, respectively. When you strip out the “Magnificent 7”[1], the P/E of the remaining 493 stocks in the index is closer to 15x.

The U.S. economy is operating at a very high level, inflation is moderating, and more people are entering the labor market. These are strong underlying supports for stocks once investor fears of the Fed recede.

– Laura G. Andersen, CFA

[1] Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla