In announcing their third rate cut for 2019 earlier this quarter, the Federal Reserve signaled that they believed this latest cut would be enough to support moderate growth and a continued buoyant job market. With the federal funds benchmark rate back down to a range of 1.5 percent to 1.75 percent, the focus now turns to whether we should expect to see rates increased again soon.

The short answer is no, and the main reason is inflation continues to remain below the Fed’s 2% target. Federal Reserve Chairman Powell stated that there would need to be a significant and persistent increase in inflation before they would consider raising rates again. Additionally, Federal Reserve Board Governor Brainard stated the recent sustained period of below-2% inflation would imply the board should also support a period of time over 2% in order to confirm inflation is now an elevated risk. Both statements are in stark contrast to the last four years, when the Federal Reserve raised rates nine times between 2015 and 2018, with inflation below their 2% target for all but a small part of 2018. Recall this time last year the stock market was in a steep decline due to investor fears the Fed would continue to increase interest rates and cause a recession. One lesson learned is the monetary policy tools of 1950-2008 may be too forceful in this era of tame inflation pressures.

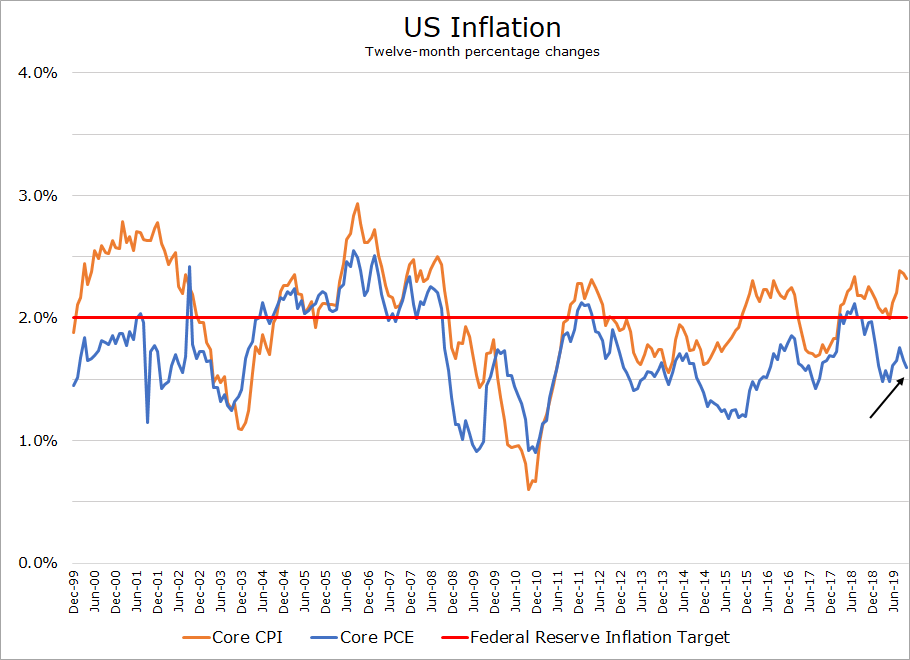

When discussing the Fed’s inflation targets, it is good to make the distinction between Consumer Price Index (CPI) and Personal Consumption Expenditures (PCE). The CPI is the index most widely followed and cited in new articles, but the PCE is the Fed’s main inflation gauge. The PCE is based on surveys of businesses as opposed to the CPI, which is a household-based survey. The PCE has generally been less volatile and has shown inflation to be lower than the CPI measure. As seen in the attached graph, the PCE came in at only 1.59% in the most recent release by the Bureau of Economic Analysis. Indeed, the core PCE (ex-food and energy) has been below 2% for most of the past 20 years.

Overall, we view this new positioning by the Federal Reserve as a positive for the market, particularly if it leads to a slower and more deliberate approach to rate increases in the future.

– John Shelbourne, CFA