U.S. stocks moved higher in May, with the S&P 500 capping off nine consecutive weeks of gains. The market’s upward momentum was fueled by red-hot artificial intelligence (AI) stocks, as investors remained largely unperturbed by continued shipping disruptions in the Strait of Hormuz. Beneath the surface, however, the S&P 500 increasingly represents a concentrated bet on AI rather than a broad barometer for the U.S. or global economy. The index now holds nearly a 50% weight in AI-related companies, a group that includes semiconductor manufacturers, cloud computing providers, and electrical equipment stocks.

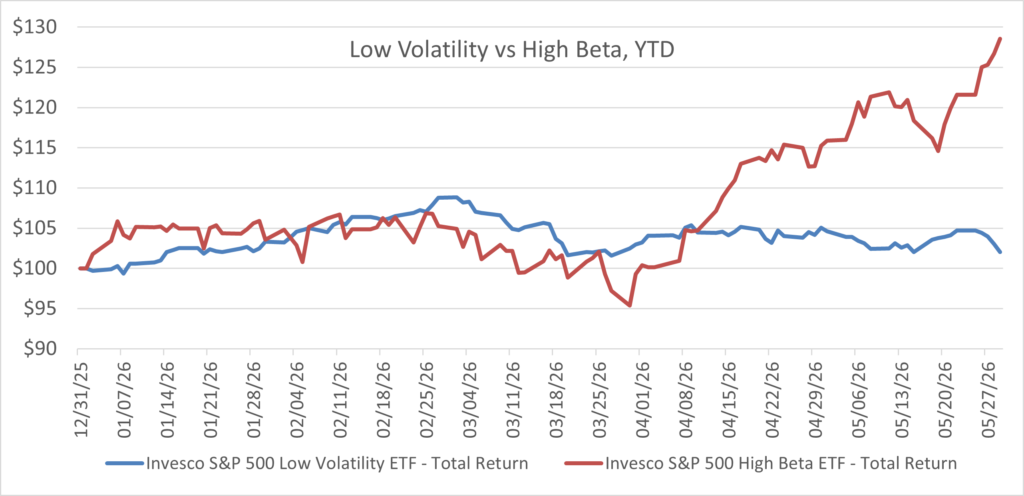

This relentless excitement around AI has ignited a strong “risk-on” appetite. Citadel Securities, the largest options market maker for retail investors, recently characterized this surge in trading activity as “performance chasing1.” Like the “K-shaped economy” of recent years, which reflected the widening gap between thriving higher-income consumers and struggling lower-income households, the stock market is now showing a similar K-shaped divergence. Higher-risk, more volatile stocks have surged, while lower-volatility, “boring” stocks have been largely passed over by investors. For example, an ETF tracking high-beta S&P 500 stocks is up over 28% year-to-date, while its low-volatility counterpart has returned just 2%. While tempting in the short term, this speculative momentum runs counter to historical norms. According to a CFA Institute Research & Policy Center post, data dating back to 1940 demonstrates that low-volatility stocks have outperformed their higher-volatility peers over the long run2.

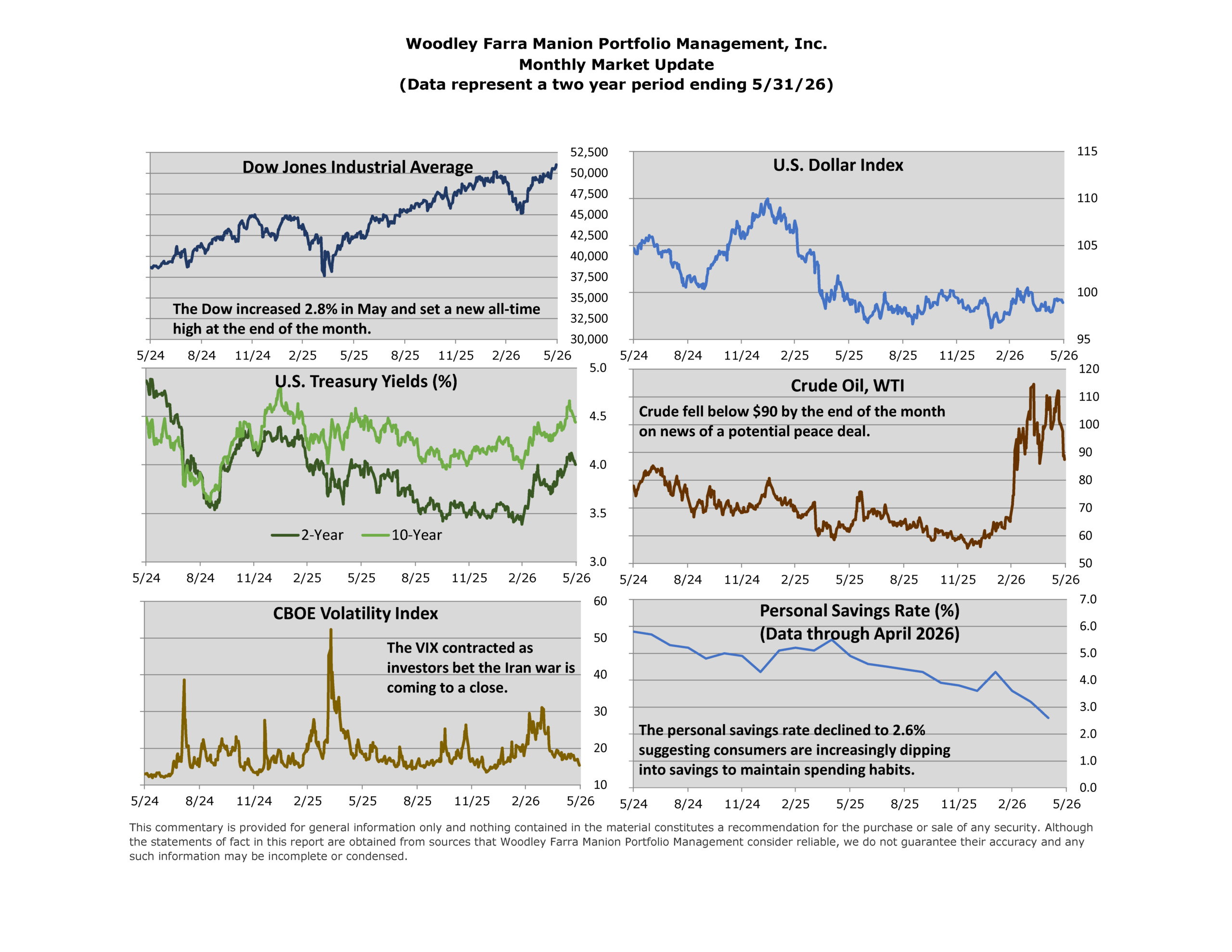

On the macroeconomic front, consumer spending remained robust in May despite the pressure of higher energy prices. Yet, this resilience comes with a notable caveat: the personal savings rate recently dipped to its lowest level since June 2022. This is a clear sign that consumers are saving a smaller percentage of their disposable income, stretching their budgets to maintain spending habits amid elevated prices and higher long-term interest rates. Moving forward, a resumption of the free flow of shipping through the Strait of Hormuz will be necessary to stabilize energy markets, restore consumer confidence, and protect household spending power.

1 https://www.citadelsecurities.com/news-and-insights/may-toolkit/

Jared J. Ruxer, CFA, MS