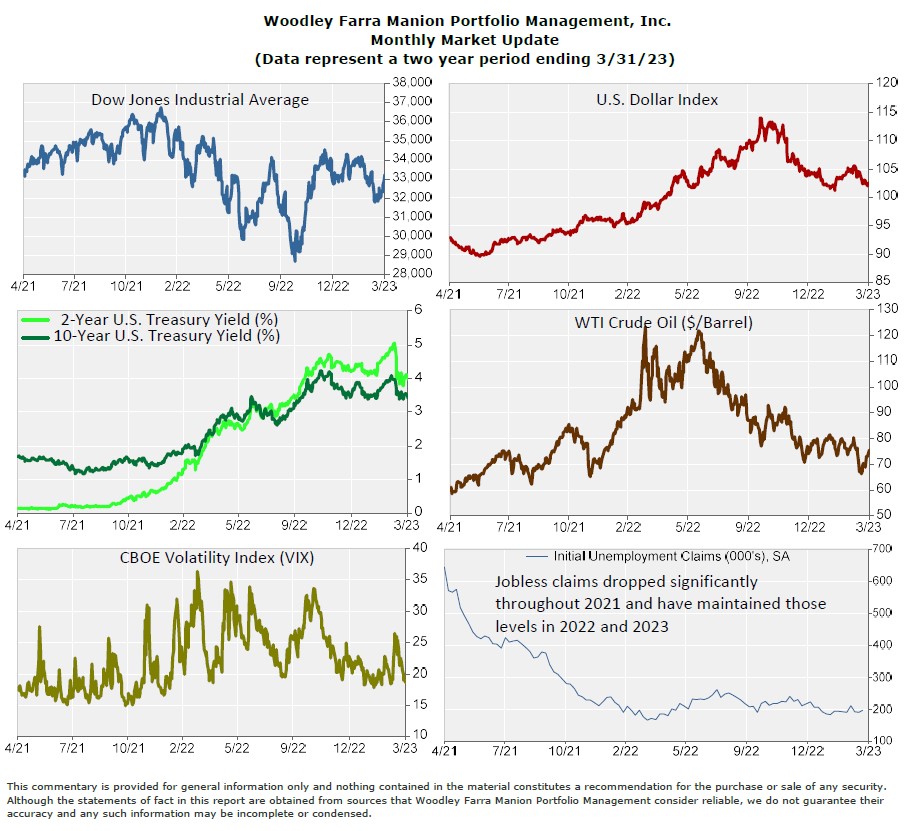

The first quarter of 2023 saw some progress in inflation data and a surge in investor enthusiasm around artificial intelligence. Nonetheless, the March failures of Silicon Valley and Signature Banks were the story of the quarter. Bank failures are not out of the ordinary. The Federal Deposit Insurance Corporation (FDIC) counts just five years without at least one bank failure going back to 1934. Most bank failures are small; Silicon Valley and Signature were the largest failures since 2008. Silicon Valley Bank’s (SVB) failure can be attributed mainly to an extreme combination of two factors. First, SVB had a risky deposit base with a heavy concentration of startup companies and venture capital firms. Over 90% of deposits exceeded FDIC insurance limits, far higher than most banks. Deposits in excess of the $250,000 FDIC limit have a strong incentive to be moved at the first whiff of trouble. Second, SVB was guilty of tremendous lapses in managing interest rate risk. SVB invested heavily in long-term fixed income securities, which experienced double-digit declines in 2022 as the Federal Reserve raised interest rates. As their depositor base of startup companies burned through cash and slowed capital raising, SVB’s deposits contracted significantly. New equity capital would need to be raised to plug the hole created by bond losses. The March 8th announcement of SVB’s proposed stock issuance brought their problems into the open. The ensuing bank run resulted in an FDIC takeover of SVB and shortly thereafter Signature, which had significant exposure to the cryptocurrency industry.

The Federal Reserve, FDIC, and Treasury’s response to backstop all deposits at SVB and Signature and open a new short-term lending arrangement with banks has since calmed markets. The Federal Reserve signaled shifting policy objectives at the March 22nd FOMC press conference with the following statement from Chairman Powell: “Since our previous FOMC meeting, economic indicators have generally come in stronger than expected, demonstrating greater momentum in economic activity and inflation. We believe, however, that events in the banking system over the past two weeks are likely to result in tighter credit conditions for households and businesses, which would in turn affect economic outcomes. It is too soon to determine the extent of these effects and therefore too soon to tell how monetary policy should respond. As a result, we no longer state that we anticipate that ongoing rate increases will be appropriate to quell inflation; instead, we now anticipate that some additional policy firming may be appropriate.” The S&P 500 stock market index ended March higher vs before the banking system events, while U.S. treasury yields fell significantly.

Recent events serve as a reminder of the importance of prudent risk management. Excessive risk taking, easily overlooked in bull markets as investors chase the hot trend, can often end poorly. Considering downside risks remains central to our portfolio management process. The bank failures also serve as a reminder to stay under FDIC insurance limits. Custodians and brokerage firms do not have claims on their clients’ securities, regardless of the institution’s financial circumstances.

Woodley Farra Manion’s Form ADV, our annual registration with the Securities and Exchange Commission, is now available. In addition, our Privacy Policy is also available. Please call or email our office if you would like to receive a copy. You can also access a copy on our disclosures page.