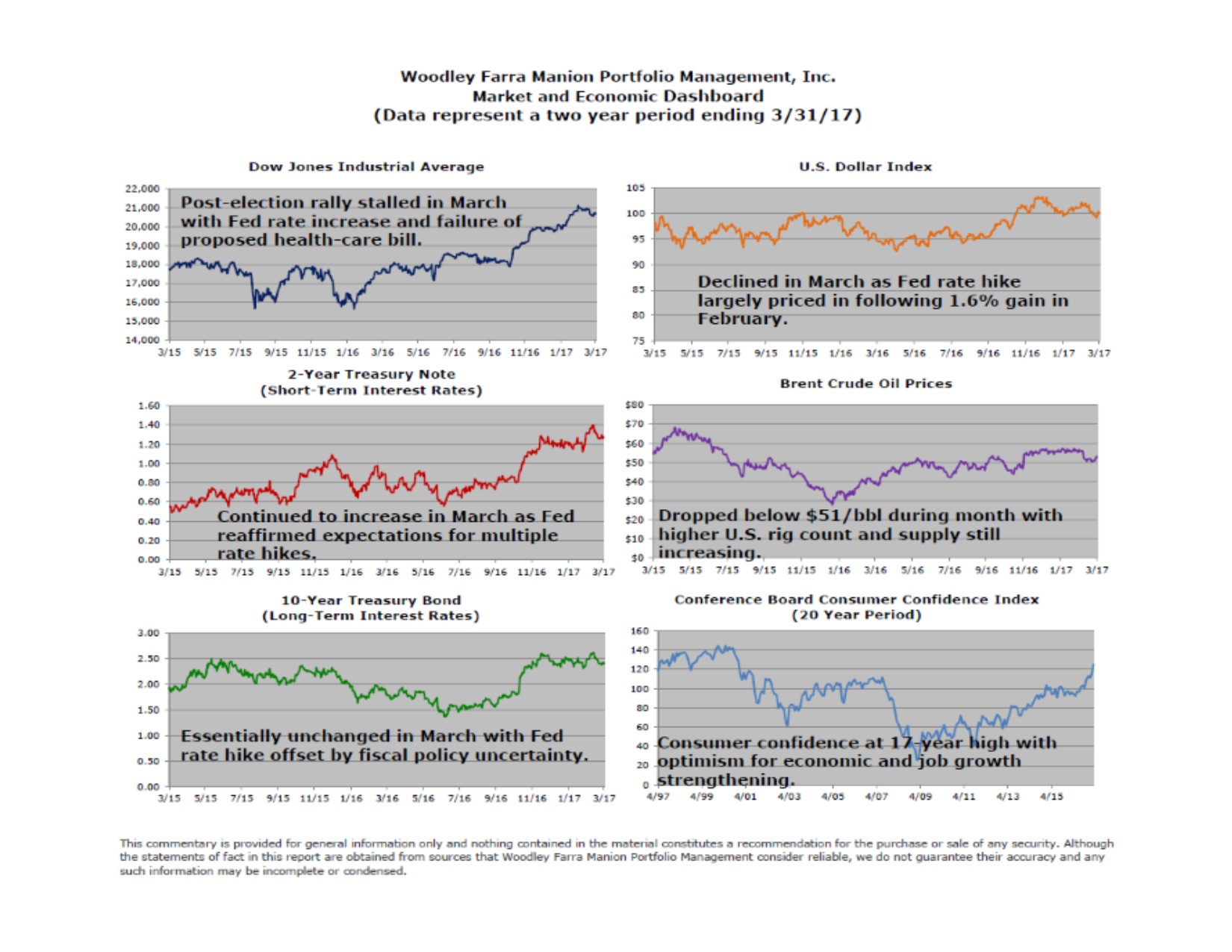

U.S. stocks continued to hit all-time highs during the first quarter, as optimism is high the economy will enter a faster phase of growth. Central to this theme is the new administration and Congress will enact legislation that will spur government spending (notably defense, homeland security and infrastructure), while reforming regulations, healthcare and taxes. Nothing notable has yet been achieved in Washington, but we expect the pace of legislation to pick up this spring and summer months.

In the meantime, the Federal Reserve increased its benchmark Federal Funds interest rate for the third time in 15 months. Investors are expecting at least two more hikes over the course of the year. Where the Fed goes after the anticipated hike in December of this year will be dependent on economic data and the level of success in Washington in the spending and reform arenas.

Surging stock prices are not just a US phenomenon. Global markets are also in a bullish mood; European stocks are at multi-year highs for several countries as years of ultra-low interest rates and modest economic reforms are taking hold. France and Germany are holding important elections later this year and the populist “Trump Effect” is being felt in both countries. It is unlikely the more populist-like parties in both countries will prevail to the extent they have in the US due to their multi-party structures and need to form coalition governments. But the “Effect” is notable as major established parties have announced more growth-oriented, freer market proposals.

Asian stocks are also higher, though Japanese stocks remain 50% below their highs achieved in 1989(!) while Chinese stocks are also down nearly 50% from highs achieved in 2007. Both countries have battled the long-term effects of weak banking and real estate sectors. Japan has been especially aggressive in trying to break the cycle of slow growth and their economy is finally starting to respond.

The global economy may finally be entering a period where every major region in the world is growing together, which has not been the case since the 1980s. The era of ultra-easy monetary policy is nearing an end and more normalized levels of interest rates are now fully expected by investors. At some point, government bonds will become more attractive for investors, but that day remains well into the future.

U.S. stocks have not had a notable correction (usually down 3%-5%) since the election in November. We do expect pullbacks in the near future, though a bear market does not appear on the horizon based on the information at hand.