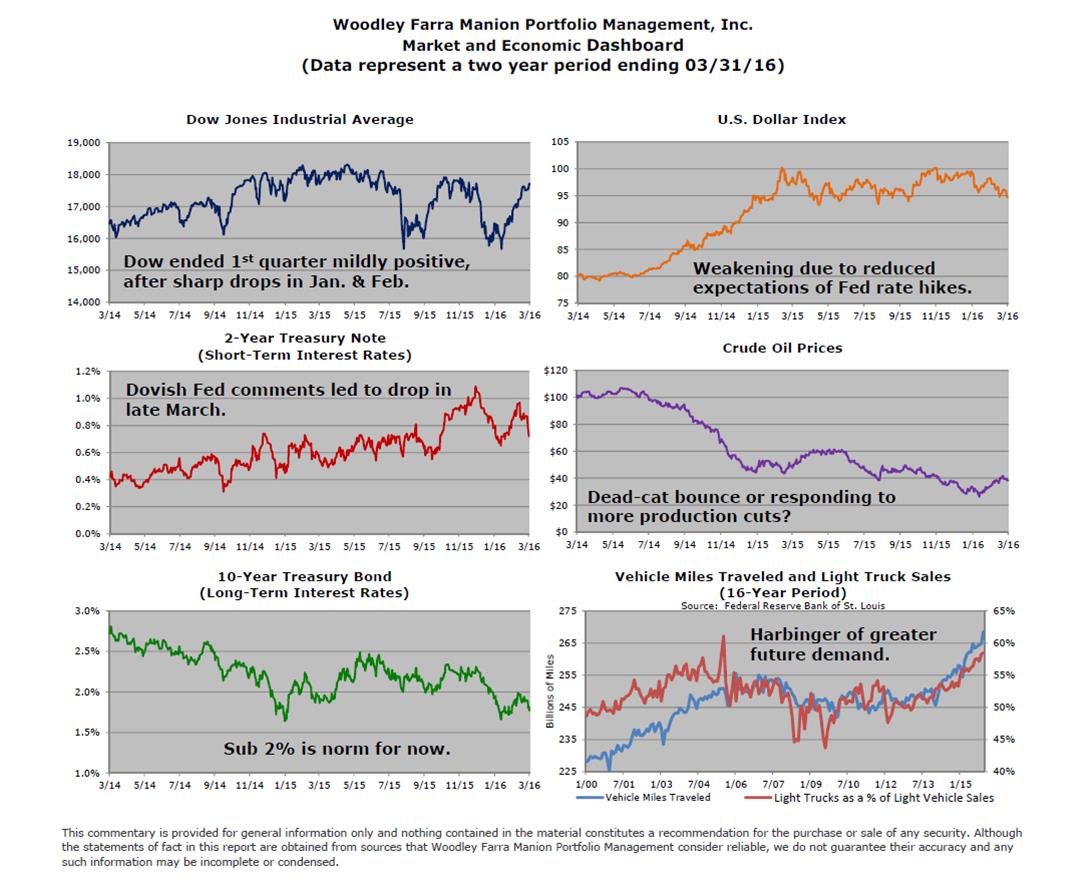

After a very rough start to the New Year, stocks staged a recovery from their lows on February 11 (the broader market was down over 11% since December 31). Besides recession fears and renewed worries about the Euro-area banking system, crude oil was the main culprit in leading the market decline and also served as the leader of its recovery. Oil had also declined 11% by February 11 and staged a 59% rally by mid-March. So the tight link seen in 2014-2015 between the fortunes of oil prices and the stock market continues into 2016.

We believe the American shale oil/natural gas revolution has been the most transformative event for the global economy in decades. The US has doubled its oil production since 2005 and can nearly match Saudi Arabia and Russia in production. The US is no longer hostage to global political swings that can push the price of oil higher. Yet, US producers are not immune to the laws of supply and demand, as other oil-producing countries increased production to force US producers to cut their output. Other than a few European oil giants, US producers are unique in the global markets by being privately owned and thus accountable to shareholders and lenders. Lower oil prices have reduced US profits; capital has naturally become scarcer and production has fallen. There will be a big shake-out among US producers and in a free market, only the strong will survive.

The benefits to US consumers have been significant. Savings at the pump (nearly $1000 per year) has allowed less-fuel efficient trucks and SUVs to account for nearly 60% of the new vehicle market. Steady economic growth has pushed the number of miles driven to new record highs. The combination of lower mileage and greater use will increase gasoline demand for the foreseeable future. Higher demand and lower production will mean oil prices below $30/barrel will not persist unless there is a significant recession in the US. Even then, eventually oil will rebound.

In the meantime stocks may not be out of the woods, having peaked in May of 2015; most stocks are down more than 20% from their individual highs and thus in their own bear market. If oil prices stay higher and the US dollar weakens, the pressure on profits will ebb and stocks will have more support to head higher. Another big drop in oil will increase the odds the market will test the February lows.