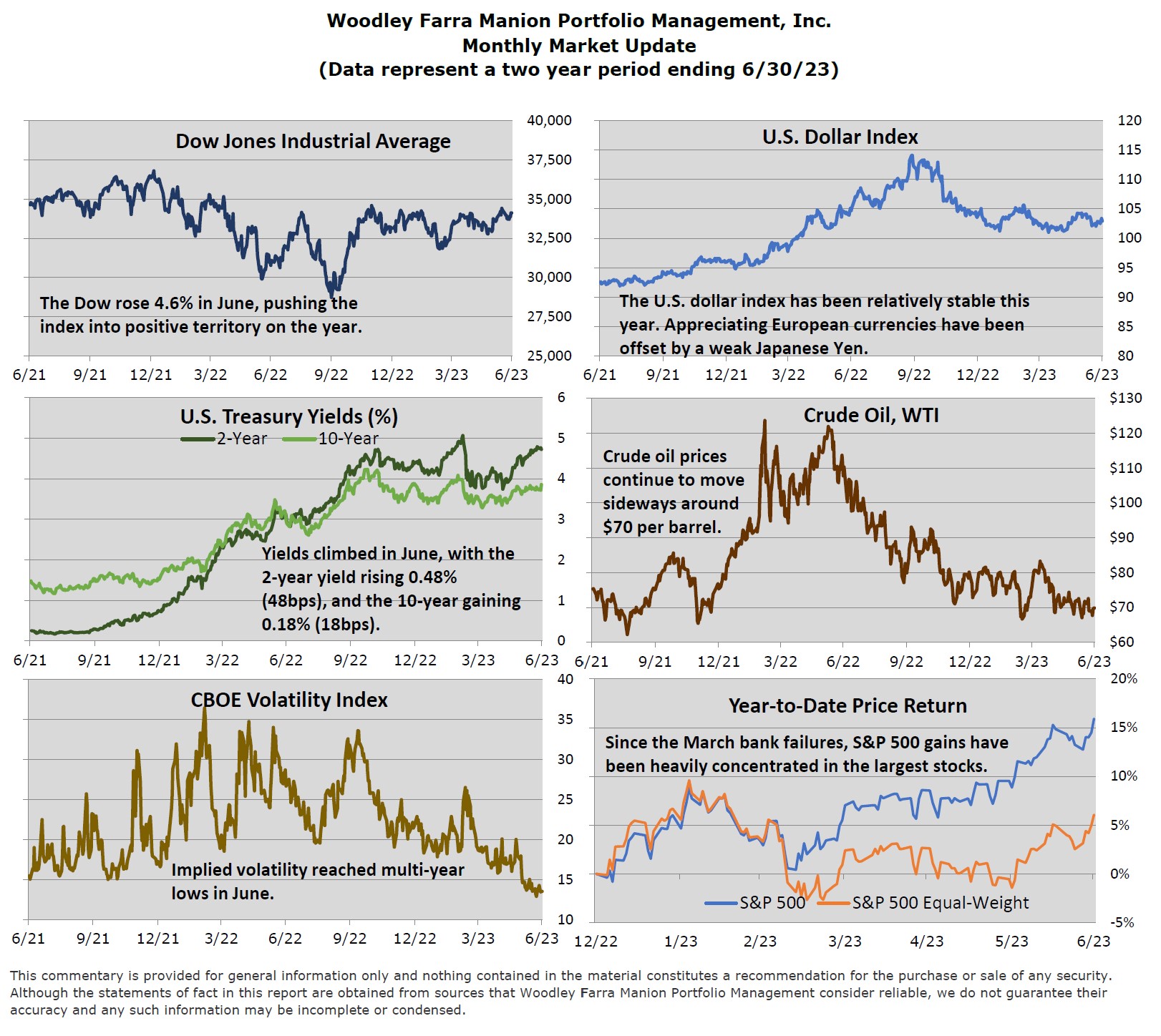

The S&P 500 stock market index rallied 8% in the second quarter, bringing year-to-date gains to 16%. The phrase “it’s a market of stocks, not a stock market” has perhaps never been more appropriate. The S&P 500 is market capitalization-weighted; meaning higher valuations hold larger weights in the index’s overall performance. More than 2/3 of the S&P 500’s gain in 2023 can be attributed to its seven largest constituents with the remaining 493 companies managing a modest return of ~5%. Broader participation among stocks and sectors is typically needed for a sustainable market rally. Continued resiliency for the U.S. economy and improving economic data in Europe could prove recessionary predictions overdone and lift a broader subset of stocks.

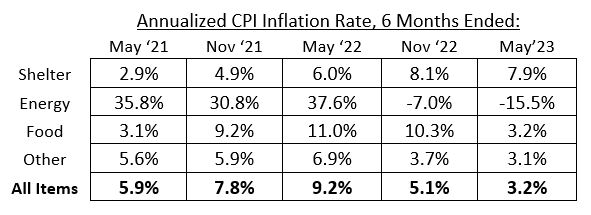

Inflation data has continued to improve since last fall. The 2022 stock market bottomed around the time core inflation (CPI ex-food & energy) peaked. Year-over-year inflation rates often receive the most attention, but below is a table of CPI growth over six-month periods (annualized) to provide a more current view of inflation. Notice the trend of disinflation (slowing inflation) in the last two periods versus accelerating inflation in the first three columns. Disinflation is providing markets greater confidence that the current rate hiking cycle could end soon. Consumers and companies are benefiting from normalizing inflation. Consumers are now seeing wages climb faster than inflation thanks in part to lower commodity prices. Stabilizing prices and improved supply chains are providing a boost to many companies’ profit margins and earnings. The U.S. dollar peaked in the fall of 2022 as the Ukraine war and ensuing energy crisis weighed heavily on currencies like the Euro and Pound. The U.S. dollar index has since declined ~10% from its peak, making multinational corporations’ foreign profits more valuable when translated back into dollars.

Covid and the Ukraine war have presented mixed economic signals, making for a unique cycle thus far. We continue to monitor at-risk segments like banks, office real estate, and the resumption of student loan payments. Economic predictions are fraught with error. Rather than assume a single outcome, we continue to maintain diversified portfolios. While valuations have expanded much faster than earnings in some of the largest S&P 500 components, we continue to see value in many areas of the market.