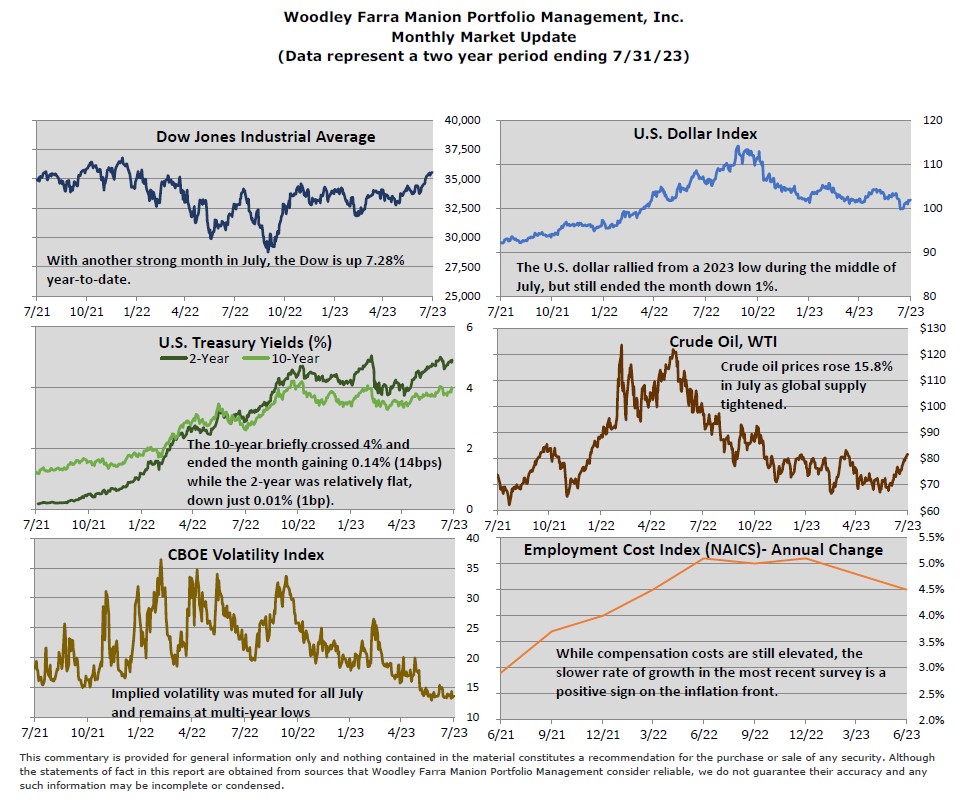

Stocks rallied in July amid low volatility with the Dow Jones Industrial Average recording 13 straight days of gains. The S&P 500 index climbed 3% on the month, on broad strength among sectors and stocks. Improving market breadth comes as a healthy change vs. the first six months of the year when the S&P 500’s gains were heavily concentrated in a few of the largest tech stocks. On July 26th, the Fed raised the benchmark interest rate 0.25%, in line with market expectations. As of month end, interest rate futures indicate it is more likely than not the Fed has reached the end of the hiking cycle.

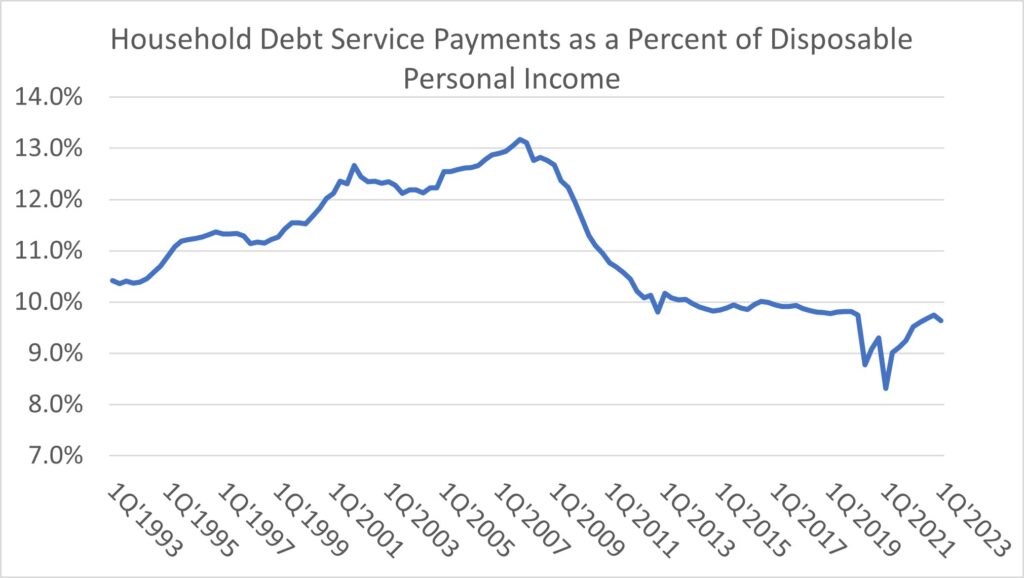

It’s been over 16 months since the first Fed rate hike, and yet higher interest rates haven’t (yet) resulted in the recession many predicted. One reason is that higher rates haven’t been felt by large parts of the economy to a significant degree. Homeowners refinanced mortgages at a record pace in 2020 and 2021, bringing the average existing mortgage rate below 4%. In contrast to fixed-rate debt like a home mortgage, which pays the same rate of interest over the term of the loan, adjustable-rate debt results in higher interest payments as market interest rates climb. When rates rise, borrowers would much prefer to hold fixed-rate debt as opposed to adjustable. As of the first quarter of 2023, just 11.1% of all household debt paid an adjustable interest rate, according to Moody’s. This number is down from 25% in 2006 and 38.9% in 1989. To state it differently, 88.9% of household debt today does not see an immediate impact when the Fed hikes rates. The chart below shows household debt service payments (interest & principal) as a percentage of disposable income. Higher debt service payments come from higher amounts of debt and/or higher interest rates. Note the ratio peaked just before the Financial Crisis in 2008 and has since normalized to very comfortable levels.

It wasn’t just consumers taking advantage of low rates in 2020 and 2021. U.S. corporations extended the maturities of debt to lock in low rates for longer, thus delaying the need to refinance maturing debt at higher rates. The Bloomberg U.S. Corporate Investment Grade index captures nearly all publicly traded debt owed by U.S. companies with solid (Investment Grade) credit. The index’s average time to maturity stood at 12.4 years in late 2021 before the Fed began raising rates, a 20-year high. Of course, there are two sides to every trade though. Buyers/lenders of long-term, fixed-rate debt have faced losses as rates rose and the value of fixed-income securities therefore fell.

It takes time for interest rate increases to impact inflation and economic growth. Households and corporations have been well-positioned to withstand and delay the impact of higher rates. This has likely contributed to the resilience of the U.S. economy despite such a large increase in interest rates.

-Jared J. Ruxer, CFA, MS