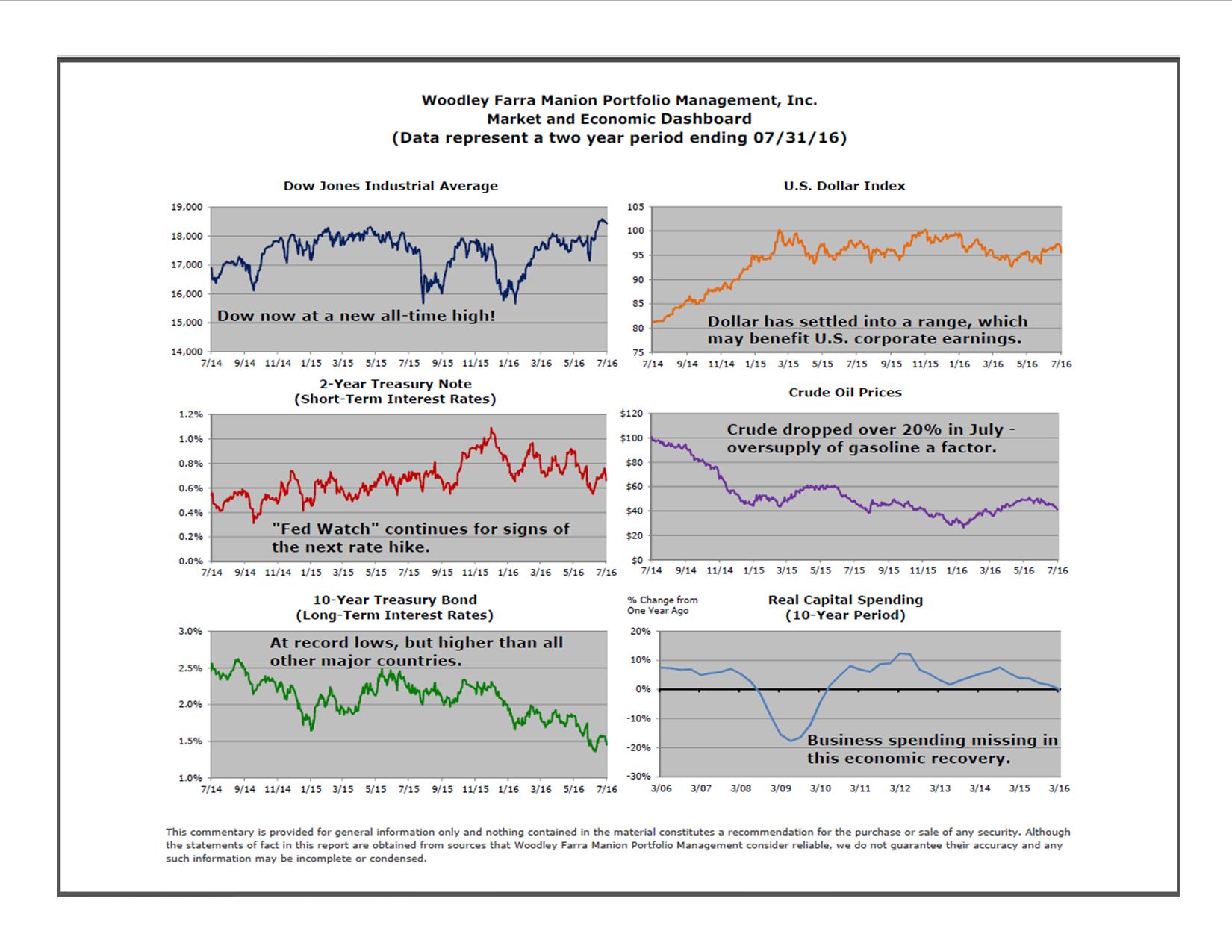

The strong (yet improbable) post-Brexit rally continued into mid-July, buoyed by a swift installation of a new government in London and improving economic indicators in the US, Europe and Japan. US stocks reached new all-time highs on July 20th, representing a rally of nearly 9% from the post-Brexit lows of June 27th. Stocks began to finally cool-off near the end of the month, taking a well-deserved breather.

The key factors behind the surge to new stock market highs include:

1. June jobs report was much better-than-expected and eased recession fears considerably.

2. Corporate profits have declined the last five quarters due to energy-related losses and a strong dollar; the recent rally in oil has ended due in large part of significant supplies of gasoline. The dollar is now in a trading range, which should not negatively impact the overseas earnings of US corporations.

3. Brexit-induced panic selling on June 24 and June 27 appears to have been a two-day wonder. The UK has formed a new government much sooner than expected and will begin the long negotiation process to leave the EU shortly – uncertainty has been reduced.

4. Sovereign interest rates have fallen to new record lows and boosted the already large advantage stocks have over bonds in terms of generating both higher income and potential capital gains.

5. US stocks had spent the past 18 months consolidating the gains from March 2009; investor sentiment was negative, which has been a contra-indicator of the next direction of stock prices.

The summer is often the worst period for stocks, as investors tend to “sell in May and go away.” This summer may be different as the momentum of the market has accelerated as the temperatures have gone up. A correction is an inevitable part of investing and investors who sold in May could use a pullback to jump back in.