The lingering effects of the severe winter of 2014 were shrugged off as the second quarter’s first read on economic growth showed an annualized gain in GDP of 4% (much better than expected), compared to an annualized decline of 2.9% for the first quarter. Economic gains were widespread for both consumer and business spending, along with higher state/local government expenditures. After so many quarters of lower than expected growth, the snapback from the winter blues is a welcome development.

We all know bad mortgages touched off the financial crisis in 2007, which was the culmination of nearly 30 years of higher and higher consumer debt burdens. The slower pace of growth in the current recovery can be traced to a concerted effort by consumers and businesses to reduce their debt obligations. This new focus on thrift has been a strong growth retardant.

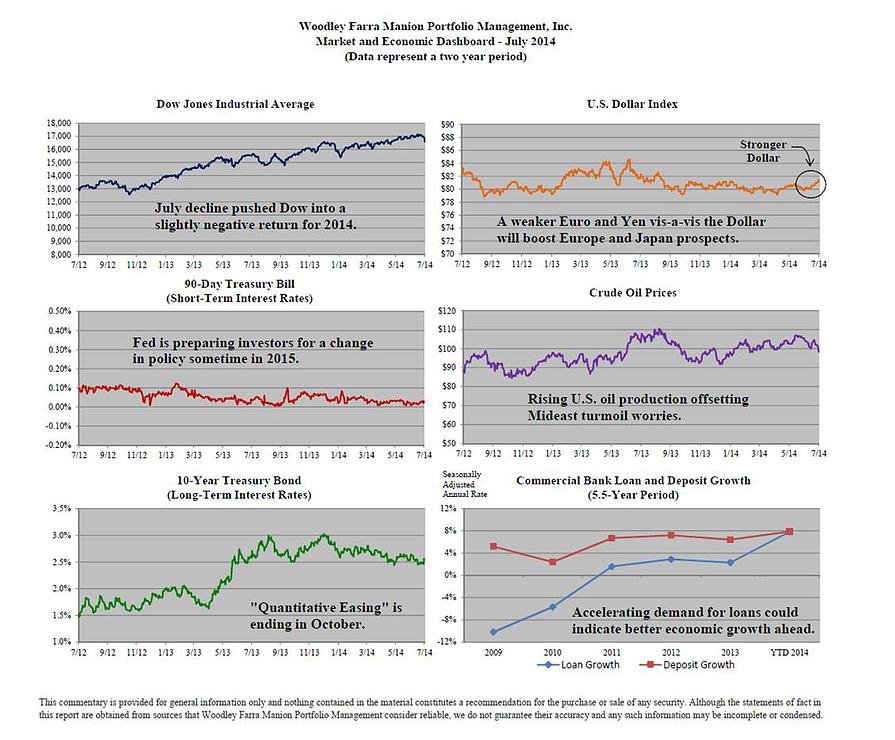

The easiest way to track attitudes toward debt is to follow the growth in bank loans. Following a dramatic drop of 12% in 2009 (a good portion of which represented bad loans), lending has begun to pick up steam. The accompanying chart in the Dashboard shows loan growth in 2014 has finally caught up to deposit growth, according to the Federal Reserve. This bodes well for the future, as the pace of economic growth appears to be durable. In addition, the Fed is beginning to condition investors to the fact that zero percent interest rates are soon to be a thing of the past.