Investors these past two Januarys may disagree with poet T.S. Eliot, who wrote that “April is the cruelest month…” Similar to the poor start in 2014, this past month saw the major indexes fall between 2% and nearly 4%. Defying the old Wall Street axiom that “as January goes, so goes the rest of the year,” 2014 turned out to be a pretty good year for the indexes. We’ll know more later if 2015 has the same bounce!

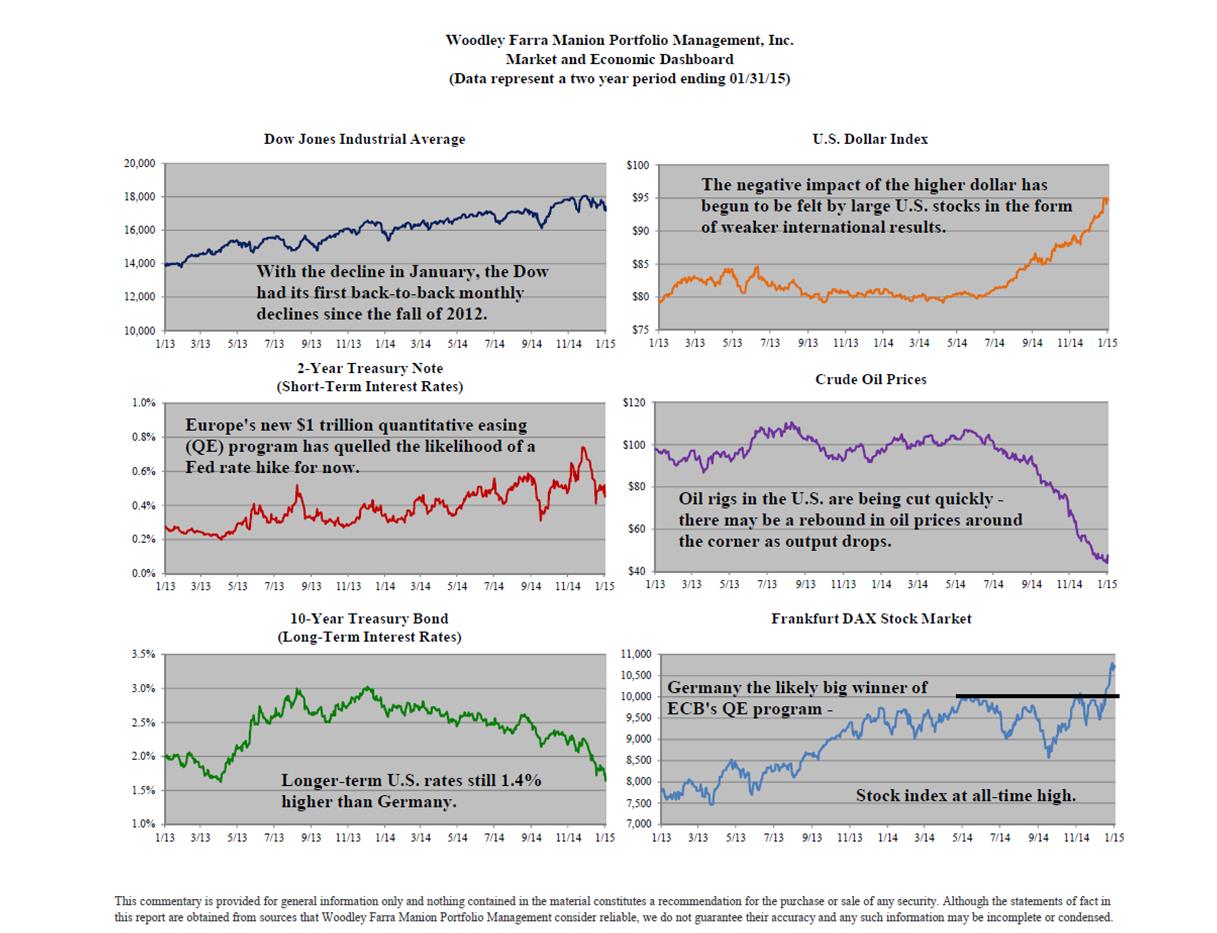

The most significant headwind that has popped up for stocks has been the strength in the value of the US dollar. The collapse in oil prices since last summer has had the coincidental effect of boosting the dollar. A significant portion of the S&P 500 and Dow 30 are multinational companies whose international sales and profits are negatively impacted when the dollar strengthens. So, while it is not a surprise many companies have blamed softer operating results this past month on the higher dollar, the market’s reaction has been the sell-off since the start of the new year.

Longer term the benefits of a stronger currency will be muted inflationary pressures (the Fed will be very patient before raising interest rates) and more capital entering the US as overseas investors pursue better returns offered by US bonds, stocks and other assets. Combined with much lower oil imports, the country’s “checkbook” will be closer to being in balance for the first time since the 90s. The strong dollar is pushing the Euro to multi-year lows, making the Euro Zone more competitive. Germany in particular should benefit the most, and its stock market, highlighted in this month’s Dashboard, is at an all-time high.