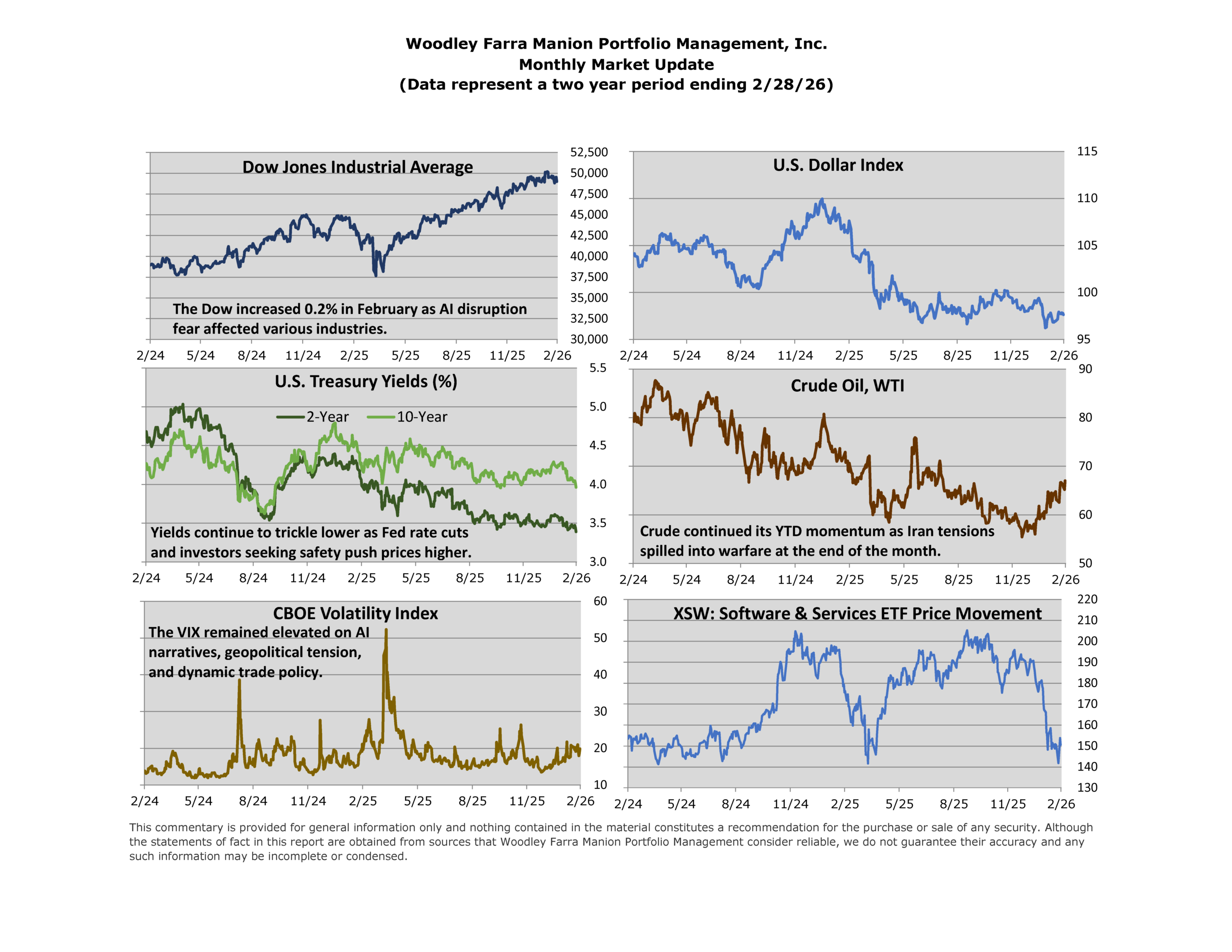

The S&P 500 declined 0.87% in February, after a modest increase in January. Market dynamics were driven less by index‑level movements and more by sector‑specific shifts. Software and consulting companies were under pressure amid rising concerns about potential disruption from accelerating advances in artificial intelligence. Losses deepened following the publication of a pessimistic AI scenario by the Substack blogger Citrini Research. These fears were counterbalanced by commentary highlighting more constructive long‑term outcomes, the challenges of meeting optimistic AI expectations, and the historical benefits of creative destruction. Supporting this perspective, Anthropic’s Claude platform announced new capabilities within Claude Cowork and partnerships with financial services firms, underscoring potential opportunities for collaboration rather than displacement.

The “broadening out” trade continued during the month, with investors rotating from mega‑cap technology into cyclical sectors. This shift was influenced by optimism around the U.S. economy’s ability to sustain strong growth in the face of elevated inflation—often referred to as the “run it hot” economy—as well as growing caution about the incremental returns on large‑scale AI capital expenditures. Year‑to‑date, the S&P 500 Equal Weight Index has risen 6.8%, outperforming the S&P 500 by 6.3%.

From a macro and geopolitical standpoint, U.S. rhetoric intensified around possible military action against Iran absent a diplomatic agreement on its nuclear program. The United States reinforced its position by deploying additional military assets to the region. Subsequent talks in Geneva appeared constructive, with Iranian officials reaffirming the peaceful intent of their nuclear activities. However, in the final days of February, the United States launched strikes against Iran, driving oil prices and defense contractor stocks higher.

International trade developments also returned to focus after the Supreme Court ruled 6–3 against the use of emergency tariff powers under the International Emergency Economic Powers Act (IEEPA). In response, the White House implemented a new 10% global tariff under a different authority and signaled the possibility of increasing it to 15%.

Meanwhile, the economic backdrop remained encouraging. Positive data surprises persisted, supported by a strong January payrolls report. Despite the robust labor market, the policy outlook remains uncertain as inflation continues to run slightly above the Federal Reserve’s target. The impact of AI driven labor market adjustments also remains an open question for future policymaking. Currently, the market is pricing in two 25 basis point rate cuts for the year, with the first expected in June.

-Nicholas Von Thomas