February was a case of good news is bad news, or to be more specific, good economic data was bad news for stocks and bonds. Economic data continues to point to a resilient US economy, shrugging off higher interest rates. Retail sales reaccelerated in recent months, with real (after inflation) incomes on the rise. Fourth quarter GDP grew at a seasonally adjusted annualized rate of 2.7%, according to the most recent estimate. First quarter 2023 GDP is expected to show similar growth1. The solid economic data drove renewed concerns of persistent inflation and, therefore, a Federal Reserve unlikely to back off rate hikes in the months ahead.

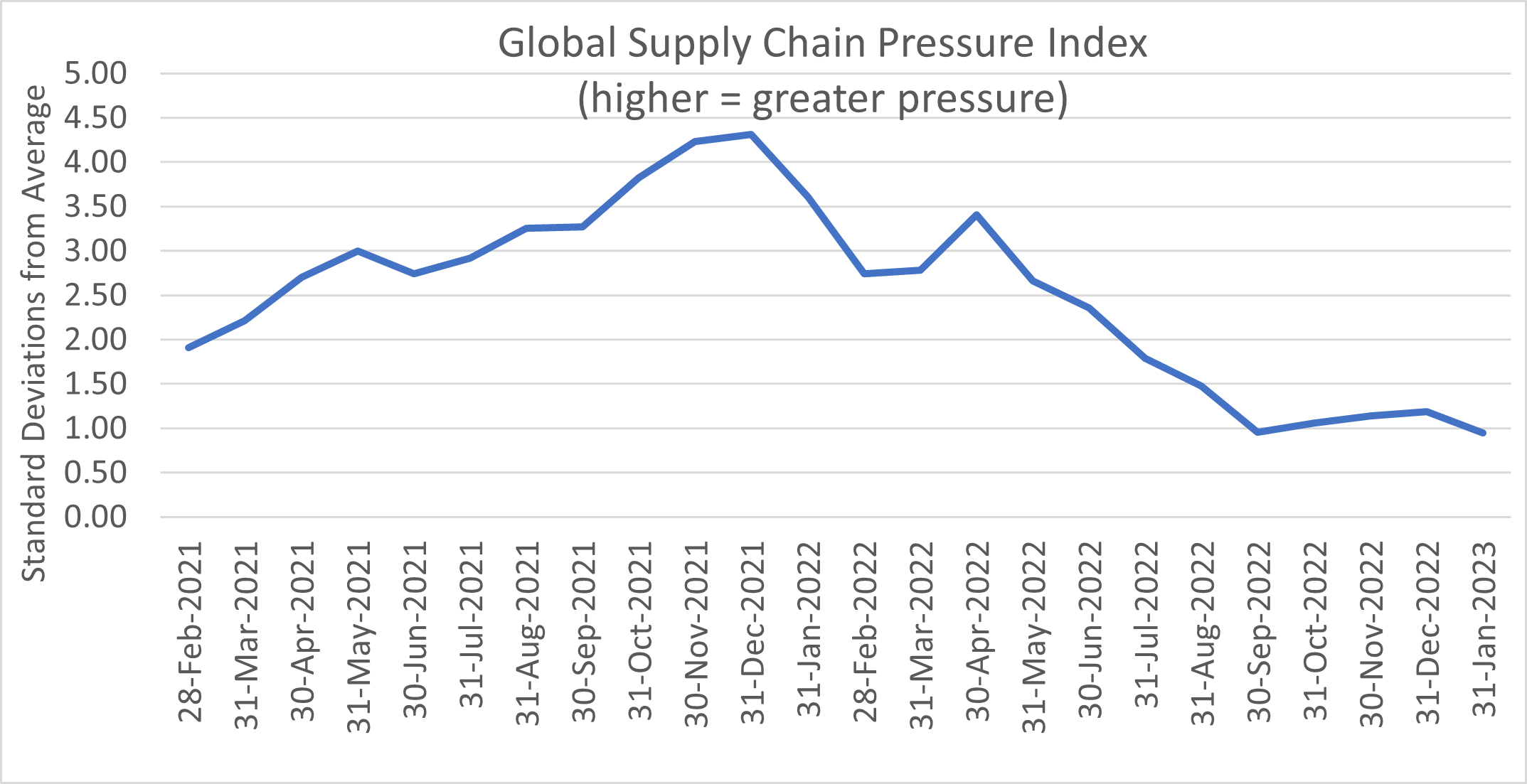

Earnings season, the period in which most companies reported their fourth quarter results and provided guidance on 2023 expectations, is now largely wrapped up. While results and expectations vary widely, executives are operating in an environment of slower revenue growth than in ’21 & ’22, but with continued cost & profit margin pressures. Nevertheless, cost pressures have abated somewhat, especially for companies more exposed to commodity costs and supply chain disruptions. Commodity prices have fallen dramatically from peaks in the first half of 2022. And the chart below shows the New York Fed’s Global Supply Chain Pressure Index2, which has moderated significantly since the end of ’21. Normalizing supply chains should help ease inflationary pressures, all else equal. Wages are proving to be a more persistent source of inflation than commodity and supply chain issues. Employment data is likely to be another example of “good news is bad news” for markets in the short term, with strong jobs and wage numbers potentially putting downward pressure on stocks and bonds.

-Jared J. Ruxer, CFA, MS