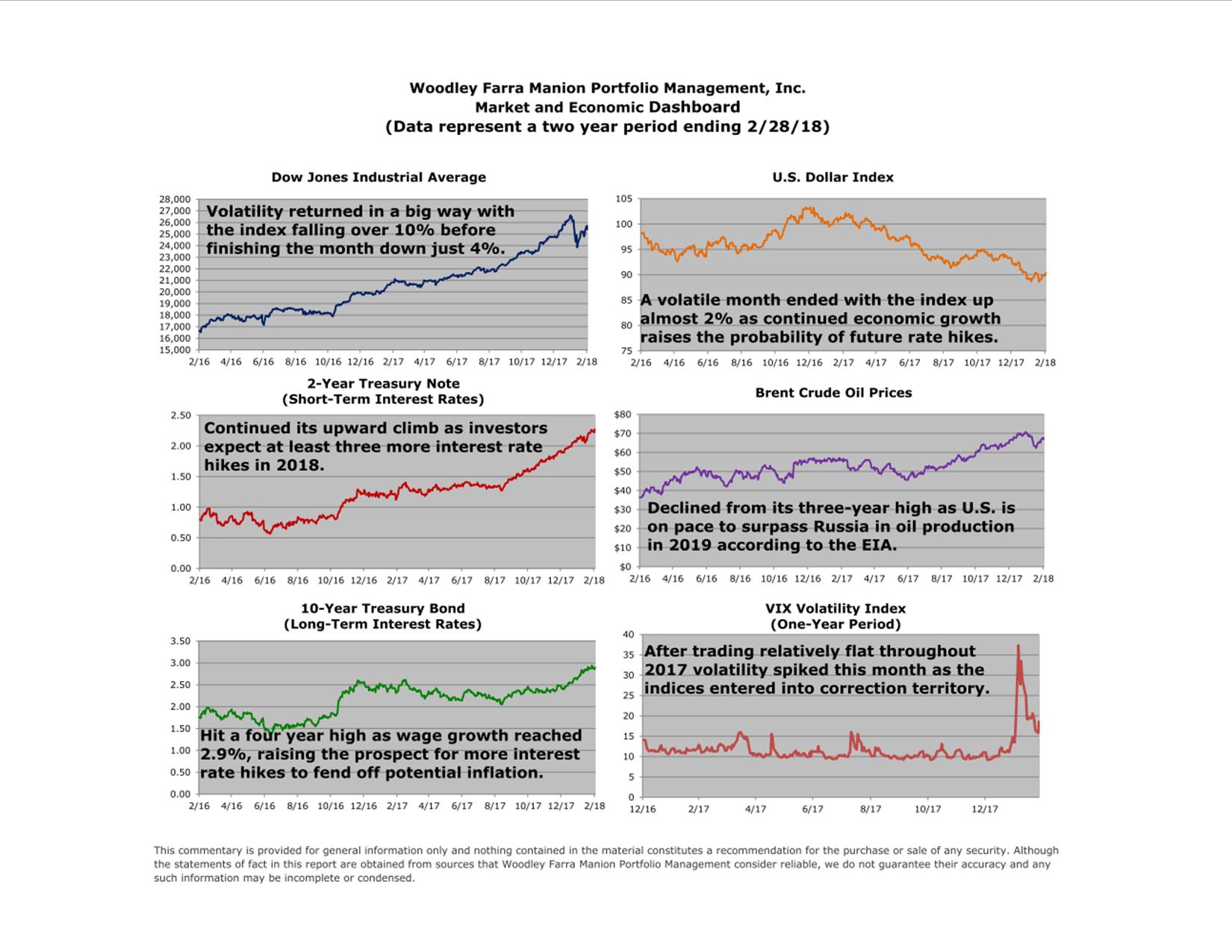

So much for another quiet year. Throughout all of 2017 the Dow Jones and S&P 500 indices never declined more than 3% from their latest highs on their way to full-year total returns in excess of 20%. The momentum continued into January as it seemed like we were on our way to another great year. But then February 2nd happened, and then February 5th happened. On Friday February 2nd the Dow Jones Industrial Average declined 2.5%, the largest single day decline since June 2016. What a great way to start the weekend, eh? Well things only got worse the following Monday when the index set a record for the largest single-day point decline in its history, 1,175 points, or 4.6%. Needless to say, volatility has returned.

For the past twenty years the annualized standard deviation (a common measure of volatility) of the Dow and S&P 500 has been around 18%, but in 2017 it was less than 7%, a post-Financial Crisis low. It’s fair to say that 2017 was an abnormal year. Despite the historically large and nerve-racking single-day declines we’ve seen so far this year, 2018 is actually off to a more “normal” start in terms of volatility, clocking in at an annualized rate around 20% so far. All of that is to say that this correction was overdue, and the volatility we’re seeing is perfectly normal.

In last month’s Dashboard we talked about the S&P 500’s historically high level above its 200-day moving average. Couple this with a move higher in interest rates and it’s no surprise that volatility spiked and stocks entered correction mode. While the 12% decline happened a lot faster than even we had anticipated, a bullish technical signal occurred when the index held at the 200-day moving average and began to recoup some of the losses. While we’re definitely paying attention to interest rates, a strong economy and lower taxes should continue to provide support to equity prices going forward.

Elliott Holden, CFA