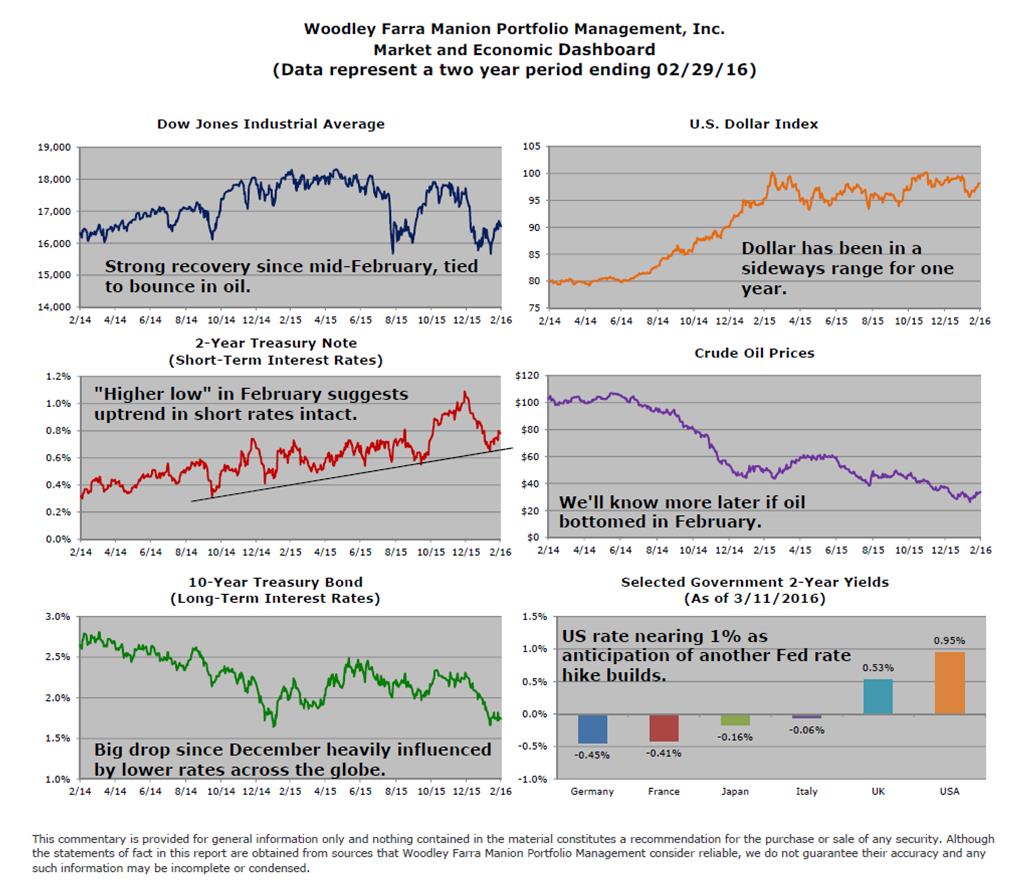

Financial markets staged a strong rally in February and early March as oil prices rebounded (the strong link with stock prices continues to persist) amid talk of OPEC members discussing coordinated cuts in their production. These rumors have popped up regularly since oil prices began their drop in mid-2014 and none have come to fruition.

In the meantime, the number of oil and gas rigs operating in the US has declined to 489, from a peak of 1,925 in October of 2014. Additionally, US land-based oil storage facilities are nearly full and offshore tankers normally used to transport oil are now being used as floating storage decks. The last line of storage options are rail cars and those are now being filled up as well. With nowhere to store oil, producers will have to relent and cut more production. Saudi Arabia’s rumored goal to force prices down to shrink the US shale producers’ market share may yet be realized.

Other than government programs that were emergency responses to the Financial Crisis in 2008 like TARP (capital injections into US banks) and the 2009 stimulus bill, the majority of the heavy lifting exerted to jump-start economic growth has been delegated to the major central banks around the world. Fiscal policy has been notably absent. The US has not attempted to reform its tax code, Europe has punted the idea of reforming labor markets and social spending, and Japan has rearranged the deck chairs on their ship of state. Central banks in Europe and Japan have now introduced negative short-term interest rates in the hope banks will be even more incented to lend money and move those economies into faster rates of growth. This policy is also hoping consumers will spend more of their savings instead of losing principal by being charged a negative rate of return.

The initial unintended consequences of this policy have been a stronger Euro and Yen and a boom in safe sales in Japan. One might as well stuff his mattress and not lose buying power rather than keep funds in a bank that deducts principal every month. The good news is the US is very unlikely to resort to negative interest rates and if economic growth does not disappoint, another rate increase or two will probably happen before the end of the year. We’ll know more later.