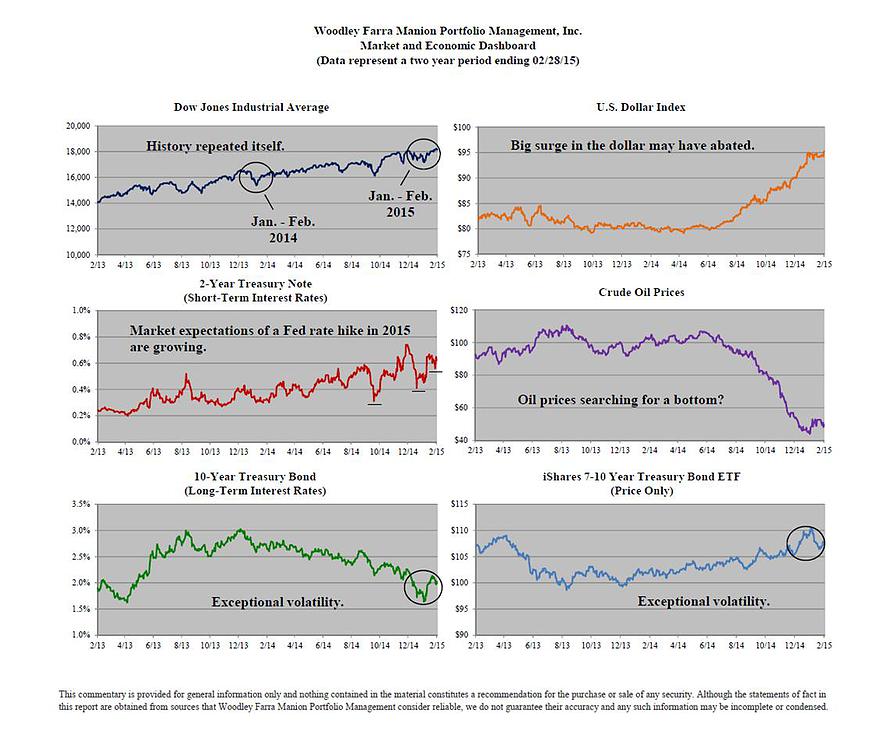

The stock market’s performance has started the New Year in much of the same manner as it did in 2014, with a large decline in January, followed by a sharp rally in February. Among the culprits for the year’s decline was the election of a new government in Greece that pledged to undo the harsh austerity program imposed by the European Union in 2011, continued drops in oil prices and an extended market condition that needed to take a breather anyway. February saw a reversal of some of these factors and the month enjoyed one of its best gains in over 17 years.

While stocks are expected to be volatile, especially since we are entering the seventh year of the current bull market, US Treasury notes and bonds have been especially volatile in 2015. An exchange traded fund (ETF) that invests in intermediate maturity Treasury notes (maturities of seven to ten years) had a price gain of 4.3% in January as rates declined sharply. Once the calendar turned to February it had a drop of nearly 2% by the end of the month, as interest rates reversed course and headed higher. This kind of yo-yo behavior is unusual.

The Federal Reserve has been diligent in communicating to investors its intention to shift its monetary policy away from the financial crisis mode of easy money and rock bottom interest rates, to a more traditional approach of raising short term interest rates to ward off any incipient signs of inflation. Rising interest rates reduce the value of bonds; it’s a simple mathematical calculation and bond investors may be coming to the conclusion the Fed is serious that 2015 will be the year policy becomes unfavorable for bond investors. Once the guessing game of when the Fed will start (June, September, a date to be named later), all investors will be focused on how high rates will go from the current level of zero and how long it will take the Fed to get to the right level that won’t hurt the economy and keep inflation pressures low.

Higher interest rates have usually been associated with better economic growth. The current pace of growth since 2007 has been sub-par relative to past recoveries, and any acceleration would be more than welcome.