2022 was the year markets were reminded of the risks posed by high inflation. Unfortunately for investors, this reminder came at a cost. Higher interest rates, intended to address high inflation, had an adverse effect on stock and bond performance. Bond prices move inversely to interest rates, so as rates rise, bond prices fall. The Bloomberg U.S. Aggregate Bond Index had its worst year on record, going back to 1976, falling 13%. The S&P 500 stock market index fell 18%. In January 2022, markets were expecting the (short-term) fed funds rate to end the year around 1%. But as the “transitory inflation” narrative lost credibility, the Federal Reserve engaged in one of the fastest U-turns in interest rate policy ever, causing the fed funds rate to blow past expectations and end the year over 4%.

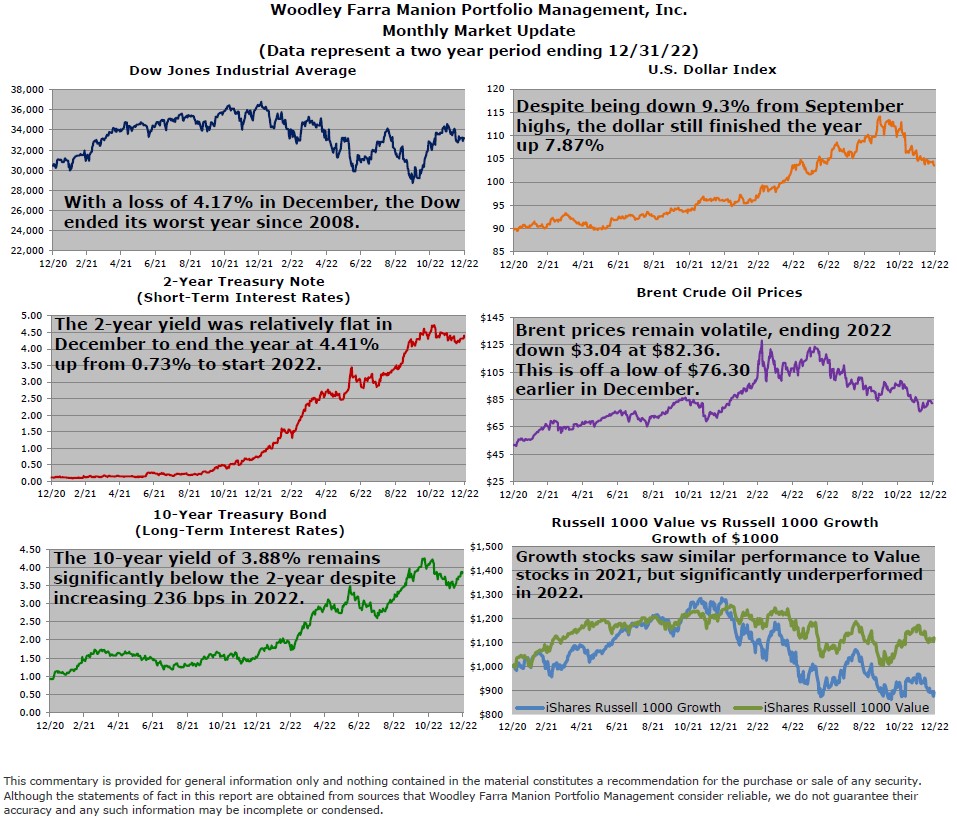

Rising interest rates and slowing economic growth contributed to a sharp reversal in risk appetites in 2022. Unprofitable growth stocks benefitted in the pre-2022 regime of low rates and abundant investor demand for risky assets (cheap capital). This environment fueled a powerful feedback loop in which companies were able to use high valuations/stock prices as a means to pay employees (keeping cash expenses low) and fund low-return growth projects. The expected growth from these projects allowed investors to justify the inflated share prices, despite their questionable potential for producing strong returns. However, interest is compensation for money’s time. At higher interest rates, patience for growth to produce cash flow wanes. This contributed to a significant fall in growth stocks in 2022. Conversely, more reasonably priced value stocks weathered 2022 relatively well. The Russell 1000 Value Index declined 8% while the Russell 1000 Growth Index fell 29%.

As inflation moderates going into 2023, a key focus will be on where it settles. Will some of the inflation prove to be very sticky, resulting in persistent mid-to-high-single-digit inflation? Or do things fall back to the pre-covid norm of around 2%? Bond markets are pricing in more of the latter. A quick normalization back to 2% inflation would be a major positive for markets and the economy, giving the Federal Reserve confidence to halt or even cut interest rates. But predicting the future is a tremendous challenge. A more worthwhile pursuit is preparation. We continue to focus on companies that can withstand a wide range of potential outcomes in 2023. We feel those with strong balance sheets, durable profit margins, favorable valuations, and shareholder-friendly management are best prepared for the coming year.

-Jared J. Ruxer, CFA, MS