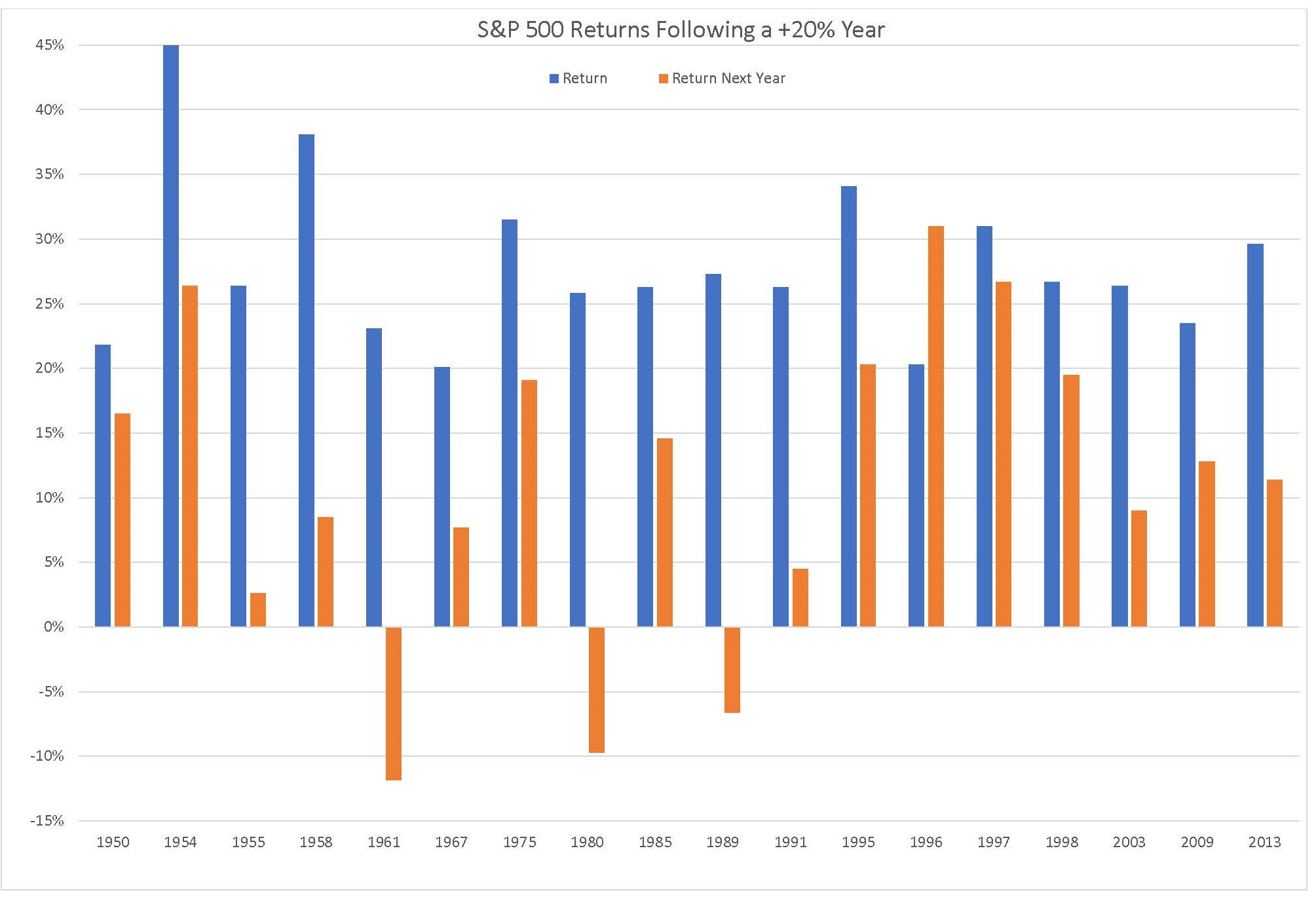

The S&P 500 is coming off one of its best years of all-time, with a price return of 28.9%. An initial reaction might be to take gains in anticipation of a pullback. History tells us such a response would be unwise, as the market has performed well following big up years. The graph below shows all years since WWII the S&P 500 price return exceeded 20% (blue line) and the following years return (orange line). The S&P has been up 15 out of 18 years following a 20% or greater gain. Historical data is limited in its ability to inform us of the future, but it does not confirm the hypothesis that big gains are followed by big losses.

Another critique of owning stocks in 2020 might be high valuations, with the most cited valuation metric being the trailing Price to Earnings (PE) multiple. A high PE multiple means investors are willing to pay up more per $1 of earnings. The S&P 500’s current PE multiple stands at 24.2x, with a historical average of 19.3x going back 50 years. This may seem high, but history shows stock valuation multiples and interest rates are closely related, as investors weigh investment options between stocks and bonds. A lower interest rate makes stocks more attractive relative to bonds, thus driving up PE multiples. Given the current low interest rate environment, we should expect valuations to be higher than periods with higher interest rates. In fact, the past four years have seen fairly stable valuation multiples, mostly within the range of 22x-25x earnings. The stock market bubble of the late 90s featured higher PE multiples than today’s despite higher interest rates, which proved to be a toxic combination.

This makes one of the market’s primary risks a sudden rise in interest rates, which would likely push down PE multiples. The Federal Reserve likely learned its lesson from the December 2018 selloff not to hike rates too quickly amid low inflation. Current low rates also mean the primary driver of healthy stock market returns going forward will be earnings growth. A flat to lower US dollar, improving trade conditions, and rebounding industrial activity are expected to lead to an acceleration in earnings growth in 2020.

-Jared J. Ruxer