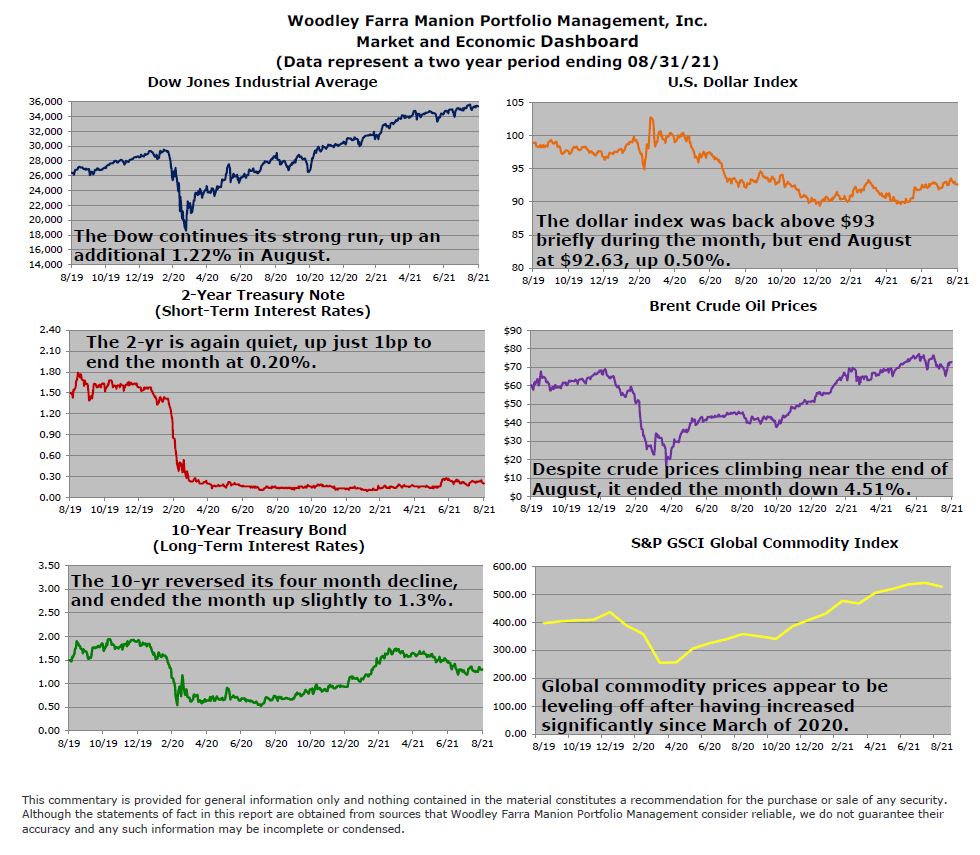

August was a relatively calm month for markets. Economic data continued to show inflation running hot, but not broad-based. Autos, especially used, account for roughly 1/3 of the rise in the consumer price index. Markets continued to shrug off inflation data. Most major indices climbed higher in August, with the S&P 500 rising 2.9%. Commodities play a crucial role in inflation as higher commodity input prices force producers to raise prices on customers. History provides a good illustration. Crude oil nearly tripled in price from mid-1973 to mid-1974 because of the Arab oil embargo. The consumer price index, which rose 3% in 1972 pre-embargo, climbed more than 10% in 1974. More recently, many key commodity prices have declined in recent months following sharp increases as economies around the world reopened. Lumber futures contracts have returned to historically normal levels following a more than 70% plunge from the May all-time high. Crude oil prices rose nearly 55% in the first half of the year, and since declined roughly 10%. Copper reached an all-time high in May, but prices have since pulled back approximately 10%. Moderating commodity prices are likely to provide some easing of inflationary pressures should the trend continue.

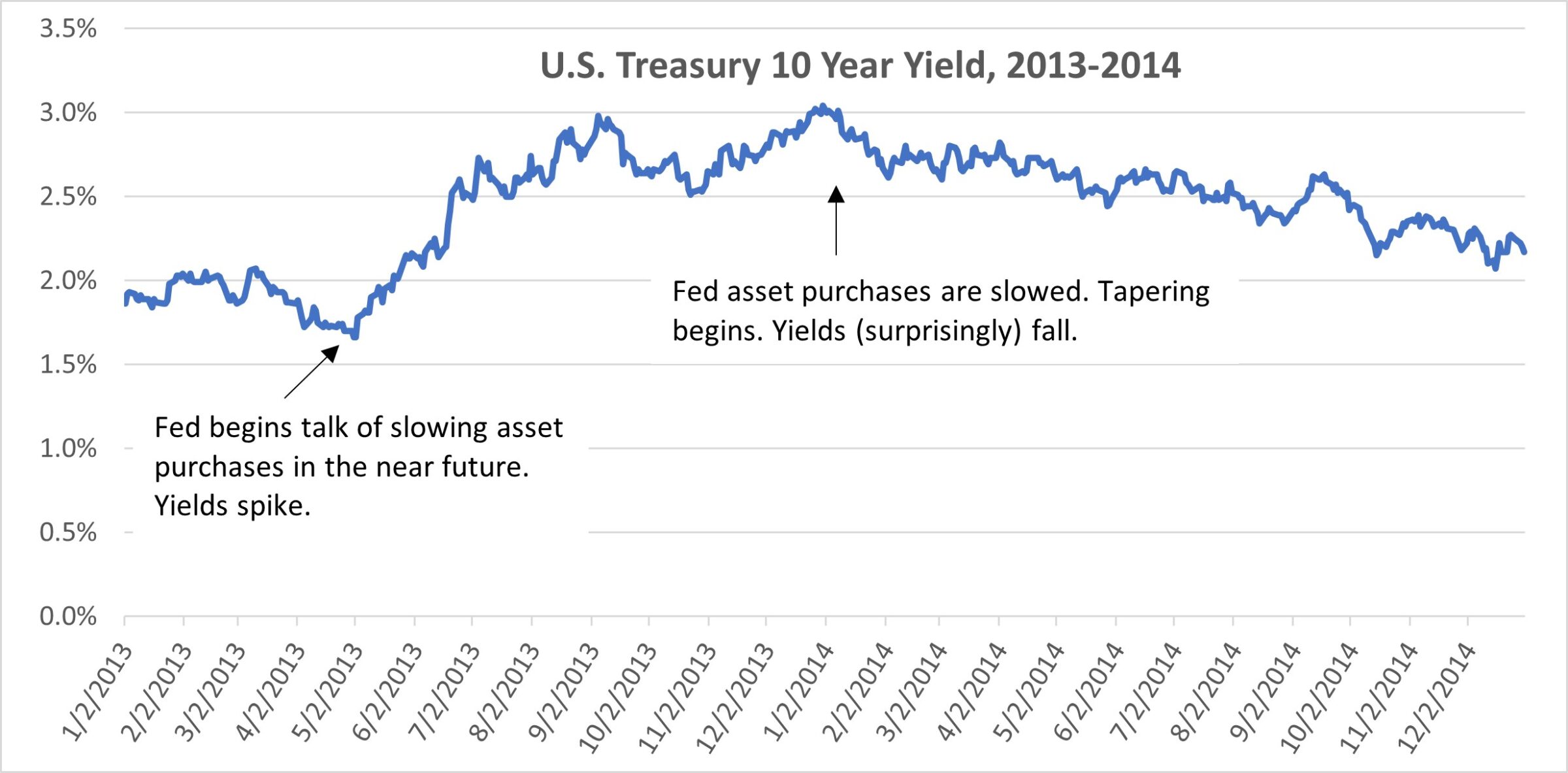

Since last summer, the Federal Reserve has been buying $120 billion in treasuries and mortgage-backed securities per month to suppress interest rates and stimulate the economy. Federal Reserve commentary has continued to shift towards tapering (slowing down) the pace of asset purchases as the jobs recovery advances and inflation runs ahead of the central bank’s 2% target. Fed Chairman Jerome Powell recently stated – “at the FOMC’s [Federal Open Market Committee] recent July meeting, I was of the view, as were most participants, that if the economy evolved broadly as anticipated, it could be appropriate to start reducing the pace of asset purchases this year”. History provides few comparisons of tapering implications for markets. The 2013 so-called “Taper Tantrum” followed the announcement of plans to taper asset purchases, resulting in a bond market selloff (and higher interest rates). Stocks shrugged off the tapering, with the S&P 500 posting total returns of 32% and 14% in 2013 and 2014, respectively.

This is not to say tapering is a positive for stocks. Markets are complex systems, with an unquantifiable number of changing variables influencing them. Fed policies and commentary are among the most important of variables but are by no means the sole driver of stock markets. We’ll know more later this year on the Fed taper plans and the potential implications for stocks and interest rates.

-Jared J. Ruxer, MS