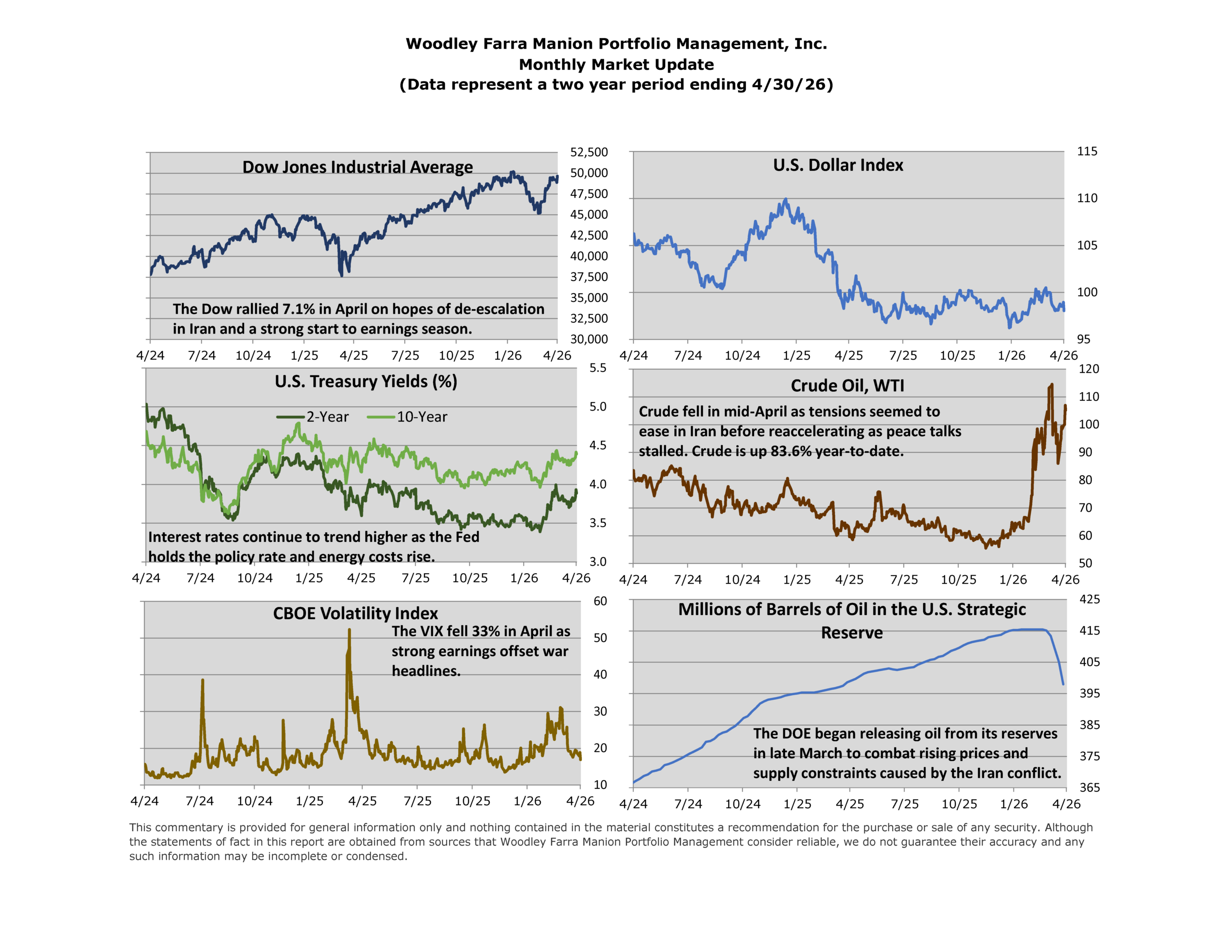

Over the past several weeks, U.S. equities generally moved higher, rebounding from an earlier slump and getting an additional lift as Middle East headlines tilted toward de-escalation. The S&P 500 (+10.42% in April) and Nasdaq (+15.29% in April) pushed to fresh highs at points, although the advance often felt narrow, with mega-cap technology and semiconductors doing much of the heavy lifting. Overall sentiment improved as oil (WTI + 7.36% in April) retreated from its spike, inflation concerns moderated, and investors gained confidence that earnings and the broader economy remain more resilient than many expected.

In our view, the month of April was primarily driven by four themes: (1) Middle East geopolitics especially Strait of Hormuz-related developments which frequently dictated day-to-day risk appetite; (2) shifting expectations for Fed policy as officials, including Chair Powell, balanced progress on inflation against growth risks; (3) macro data that continued to suggest a fairly resilient consumer and labor market; and (4) Improving sentiment heading into and during earnings season. Inflation readings were mixed but included some encouraging signals in the core data (for example, core PPI), while jobs and spending indicators did not point to meaningful deterioration. Earnings expectations remained constructive, with the market looking for another period of strong profit growth, and results were supportive enough to keep the broader bullish narrative intact despite headline-driven volatility. Notably, M&A activity also continued to surface, reinforcing the view that corporate confidence and dealmaking have not shut down.

From a leadership perspective, risk-on areas outperformed, led by Big Tech and AI-adjacent names. Different parts of the mega-cap complex took turns at the front including META +6.8%, AMZN +27.3%, MSFT +10.2%, and GOOGL +33.9%, while semiconductors and memory remained consistently strong. Small caps (Russell 2000) participated at times, but overall breadth was uneven, and the equal-weight S&P 500 lagged later in the month. Outside of technology and semiconductors, there were pockets of strength in managed care, machinery/industrials, transports, and select financials (including banks and credit cards). Energy was a key swing factor: it surged when war-risk premia and Hormuz disruption concerns rose, then gave back a significant portion of that move as ceasefire expectations firmed. Rates and the dollar were also influenced by the commodity backdrop. Treasury yields moved around but generally reflected greater comfort with the inflation outlook as oil declined. The dollar was modestly weaker during parts of the period (DXY down in some weeks), although it rebounded in the back half of the month. Oil was the most volatile asset: at one point, WTI jumped to its highest level since mid-2022 on conflict concerns, before posting its biggest weekly drop since 2022 as tensions cooled. Gold and silver tended to rebound during the more risk-off moments.

– Nicholas Von Thomas